Executive Summary

The November 3, 2020 elections produced a wholly unsatisfying result for financial advisors and their clients from a financial planning perspective, regardless of their political affiliation. The political clarity – leading to planning clarity – that many had hoped for, did not emerge. Instead, control of the US Senate, which will determine whether Democrats can drive their legislative agenda or if Republicans will have a ‘check’ over a Democratic-controlled White House and House of Representatives that could lead to gridlock instead, continues to hang in the balance.

The problem? The control-determining Senate races won’t be decided until a Georgia run-off on January 5th of 2021… which is too late to take most actions that influence a client’s 2020 tax bill! Thus, planners are left with a substantial dilemma: act now and make potential changes that could be costly and/or unwanted if substantial changes to the tax code are not implemented for 2021, or wait and risk the chance that such changes may be implemented, potentially dramatically increasing costs.

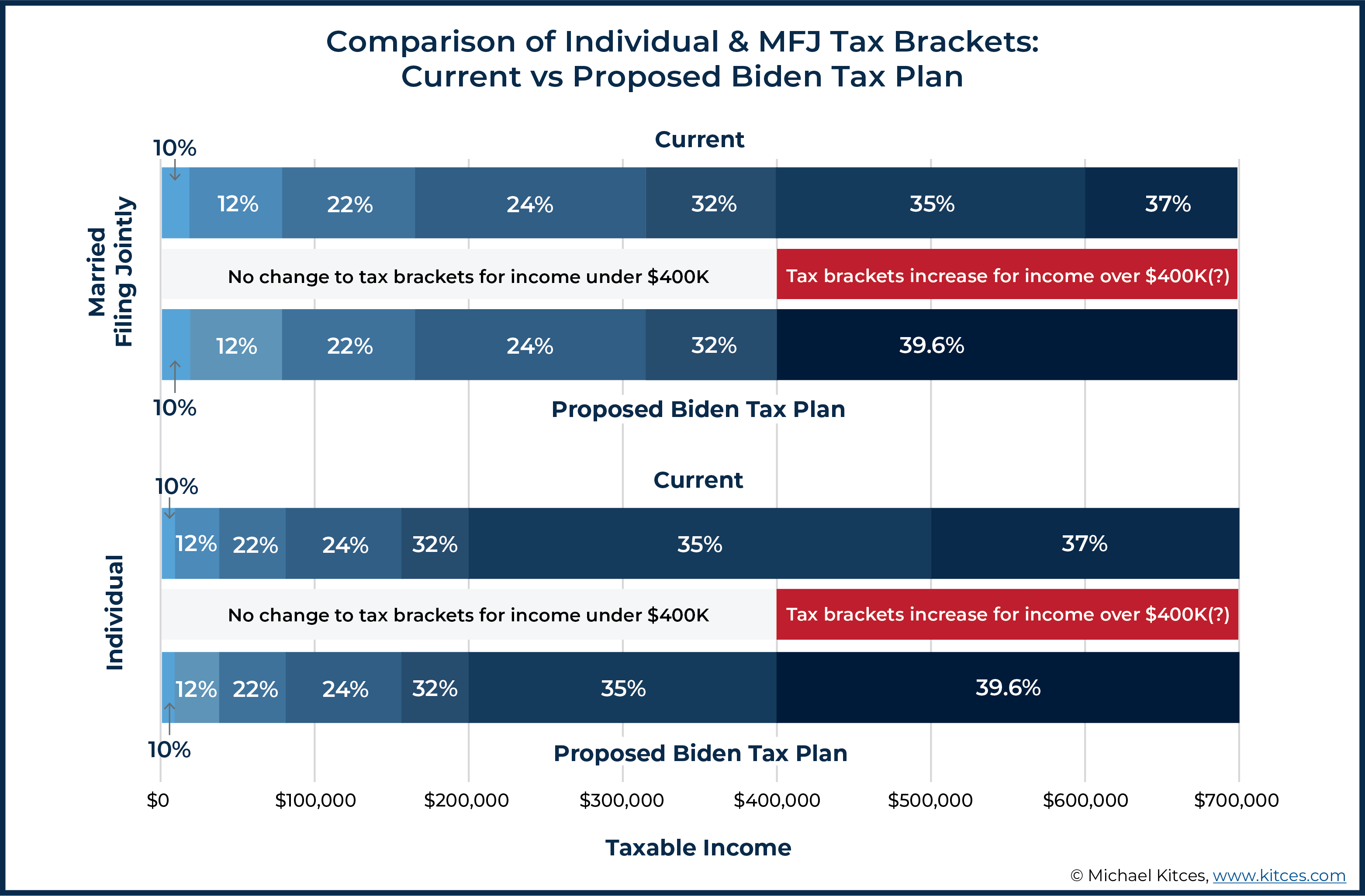

Given President-elect Biden’s proposal to increase the ordinary income tax rate for those making more than $400,000 per year, and to make the long-term capital gains rate equal to the ordinary income tax rate for income in excess of $1 million, many taxpayers and planners have considered the possibility of accelerating income for high earners into 2020. Problematically, clients who are just slightly above the threshold may actually have the most to lose with potential tax bracket changes, but also the most adverse impact if they accelerate significant amounts of income but no changes occur… while those significantly above the threshold have less potential benefit for accelerating income, but if they’re already in the top tax bracket, there’s limited downside to accelerating income even if tax brackets aren’t changed (and still some benefit if the Biden tax plan is implemented).

With respect to a change in the top long-term capital gains rate, if one is to believe that the Biden-platform income figure of $1 million is ‘real’, the decision of whether to sell or hold positions with existing gains is more nuanced. On one hand, the cost of selling such investments in 2020 (i.e., harvesting capital gains in the current tax year before the increase) would trigger a 20% long-term capital gains tax that might be a tough pill to swallow. But should the Biden proposal become law, it would nearly double the current top long-term capital gains rate from 20% to 39.6%! Which means those with very high income or especially sizable capital gains may still want to take some chips off the table with year-end capital gains harvesting, if only as a form of “tax insurance” to hedge against the risk of potentially dramatic increases in long-term capital gains rates next year.

But, as if that decision wasn’t complicated enough on its own, further complexity is added to the mix when considering the additional Biden tax proposal calling for the elimination of the step-up in basis of capital assets upon death. Ironically, holding appreciated assets until death would rapidly switch from a very desirable tax strategy to an especially undesirable one (because taxing all appreciated investments at death, all at once, would be even more likely to push capital gains into the new higher capital gains rate!).

As the end of the year approaches, clients must also make decisions with respect to expenses that may qualify for itemized deductions. As while in general, a potential tax increase next year means there is a benefit to accelerate income (into 2020’s lower tax rates) and defer deductions (when they’d be more valuable at 2021’s higher tax rates), in practice most high-income taxpayers who already itemize deductions will benefit more by claiming their deductions in 2020 at current rates, due to the potential of the Biden-proposed cap of 28% on the value of itemized deductions! Meanwhile, clients of all income levels should still defer any expenses that won’t be counted as an itemized deduction in 2020 (such as SALT expenses in excess of $10,000, or any potential itemized deductions if the taxpayer’s standard deduction will still exceed their itemized deductions), but at least have the chance of helping boost deductions in 2021 if the rules are changed.

Finally, while the overwhelming majority of taxpayers won’t have to worry about estate and gift taxes whether the exemption remains at its current level, or is dropped back down to its pre-TCJA level as called for by the Biden proposal, advisors must address the ‘lucky’ few clients who do still face Federal estate tax exposure. Though obstacles loom large, for clients who have a net worth that will almost certainly subject their estate to an estate tax liability upon their passing (or may grow to that point in the future), there is a strong impetus to act now and engage in potentially substantial year-end gifting – up to their entire $11.58 million Federal estate tax exemption amount, to ensure they do not lose out on maximizing the current exemption while it lasts.

Ultimately, the key point is that now that the election has passed, clients are looking for guidance as to what they should be doing – or not doing – before the end of 2020 and beyond. And while in many cases, the ‘right’ answer may not be able to be definitively known today, not having a conversation about it at all is decidedly the wrong ‘move’ for proactive advisors seeking to reassure and inform clients.

On November 3, 2020, elections were held throughout the United States. While the majority of positions filled by voters that day were for state and local governments, U.S. citizens were also tasked with selecting the individual to lead our country as President for the next four years. Additionally, 33 seats in the U.S. Senate were up for grabs, along with all 435 seats in the U.S. House of Representatives. Accordingly, the balance of power in the United States was ‘in play’ on election night, leaving proactive planners hanging on the edge of their seats wondering what 2020 year-end planning would – or should – look like.

If Republicans were able to recapture control of the U.S. House of Representatives while maintaining control of the U.S. Senate and Office of the President, the lower income tax rates and increased estate and gift tax exemption created by the (Republican-passed) Tax Cuts and Jobs Act of 2017 would almost certainly be extended, with even further cuts to the long-capital gains rate and middle-class income taxes a real possibility. Accordingly, if the election had produced such a result, there would have been little to no need to take extraordinary actions to utilize the currently-high estate and gift tax exemption (because it wouldn’t be lowered in 2021) or to accelerate income into 2020 (because the income tax rates currently in force would have remained in place through at least 2022 when House seats will once again be on the ballot).

By contrast, if the November 3, 2020 results showed that Democrats held the House and flipped the Office of the President, along with the Senate, it would have been reasonable to forecast that higher rates (at least/especially for upper-income households, including the clients of many financial advisors) and a potential reduction to the estate and gift tax exemption would be on the horizon, given the proposed tax plan that then-candidate Biden proposed from the campaign trail earlier this fall.

And finally, if it were clear that there would be a split government, in which Republicans and Democrats each controlled at least one of the Houses of Congress or the Office of the President, planners could have realistically forecast few major changes to the Internal Revenue Code, owing to the dramatic differences between the parties on tax policy (which makes “gridlock” the likely outcome of any substantial proposed tax legislation).

Unfortunately, from a planner’s perspective, the November 3, 2020 elections produced a wholly unsatisfying ending. Rather than providing the certainty that planners had yearned for throughout the first 10 months of 2020, the (current) results largely leave the fate of the Internal Revenue Code up in the air.

More specifically, despite lingering legal challenges from the Trump campaign, it is now all but certain that former Vice President, and now President-Elect Joe Biden, will assume the role of President of the United States on January 20, 2021. Furthermore, despite unexpectedly losing a number of seats, Democrats managed to hang onto control of the U. S. House of Representatives.

Control of the US Senate, however, continues to hang in the balance. Currently, Republicans are presumed to retain control over 50 seats. Democrats, on the other hand, together with the Independents who caucus along with them, are presumed to control 48 seats. The remaining two seats – oddly enough, both in Georgia – are to be determined in a run-off.

If Republicans can take at least one of those seats, they will retain control of the Senate, in which case dramatic changes to tax policy are unlikely to occur in 2021. If, on the other hand, Democrats are able to nab both seats, it would create a 50-50 split. And in the event of a tie in the Senate, the deciding vote would be cast by Vice President-Elect, Kamala Harris… effectively giving the Democrats a majority vote in the Senate (to complement their control of the House of Representatives and the White House), and thus leaving the door to major changes to the tax rules for 2021 wide open.

The problem? The Georgia run-offs are not going to take place until January 5, 2021… which is too late to take most actions that influence a client’s 2020 tax bill! Of course, even if significant changes are made by a fully Democrat-controlled U.S. Government in 2021, there’s no guarantee they would make those changes effective for 2021. Instead, they could make such changes effective only for prospective tax years, beginning in 2022. Or not…

And thus, the problem. Advisors and their clients are left with a substantial dilemma in light of the 2020 election results and the fast-approaching end of the year: act now and make potential changes that could be costly and/or unwanted if substantial changes to the tax code are not implemented for 2021, or wait and risk the chance that such changes may be implemented, potentially dramatically increasing costs.

Should Clients Accelerate Income Into 2020 Before A Potential Democrat Tax Increase?

If Democrats are able to win both runoffs in Georgia in January 2021, the prospects for higher income tax rates in the near future rise dramatically, especially for those with high income. Notably, President-Elect Biden’s platform included proposed increases to the ordinary income tax rates for taxpayers with income in excess of $400,000, along with changing the long-term capital gains rate from the current top rate of 20% to ordinary income tax rates for those with over $1 million of income. The Biden platform also included a proposal to eliminate the step-up in basis for capital assets upon death, and to make death a realization event (as though any/all appreciated investments were sold on the date of death), resulting in the taxation at death of all yet-to-be-realized capital gains.

Given these potential changes, many taxpayers and planners have considered the possibility of accelerating income into 2020, as the current (low?) rates are at least known.

Notably, though, even in a completely Democrat-controlled Washington, for taxpayers whose income is expected to be less than $400,000 for the foreseeable future, the likelihood of ordinary income tax rates increasing in 2021 is fairly modest (given that the Biden proposal very explicitly targeted $400,000 as the income threshold at which higher tax rates would begin to apply).

On the other hand, that means today’s tax rates are much less certain for those with income in excess of that $400,000 amount, making it more appealing to at least consider accelerating income for those with income above $400,000 (and especially those in the top 37% tax bracket, as even if tax rates are not changed next year, there’s limited downside to accelerating income for those who are otherwise pegged to the top tax bracket, anyway!

Nerd Note:

Because the Biden Tax Plan shared on the campaign trail was only that – a high-level tax plan, but not a specific proposed legislation – the details of how new tax brackets would apply remains to be seen. Even with respect to the prospective $400,000 threshold, it’s not currently clear whether that threshold will apply for both individuals and married couples, or whether the threshold might be different for each (e.g., $400,000 for individuals but higher for married couples, to at least partially mitigate the marriage tax penalty that would otherwise occur).

Strategies To Accelerate Income For High-Income Households

While there are many ways to do so, one of the most common ways for taxpayers to accelerate ordinary income is via (partial) Roth conversions. After all, in order to ‘pull’ ordinary income into 2020, there has to be income available to pull. Retirement accounts represent a logical place from which to pull such income, and if you’re going to voluntarily pay income tax on retirement account distributions that are not needed today, why not put those dollars in a Roth IRA to allow them to grow tax-free for the future?

Perhaps somewhat ironically, accelerating income in a situation like this would have been much easier prior to the Republican-passed Tax Cuts And Jobs Act. Notably, it was that act that eliminated the ability for taxpayers to recharacterize such a conversion (up to October 15 of the year following the year in which the conversion was made). With the elimination of that provision, the decision to accelerate income into 2020 via a Roth is much more complicated than it was in the past when potential tax hikes were on the horizon. Previously, clients might have conducted a sizable Roth conversion, then waited to see what happened, and simply recharacterized after the outcome of the Georgia run-offs (and any potential 2021 tax legislation) was clear. But now a Roth conversion is an irrevocable decision, the results of which clients must live with, which means the decision has to be made upfront before the end of this year.

Other clients who may have the ability to accelerate income into 2020 are business owners. In some cases, cash-basis business owners are able to accelerate certain billing, such that more income is collected and received in 2020. In other instances, the same businesses can delay paying certain expenses until the beginning of 2021, in order to increase taxable income in 2020 (as a result of fewer deductions that weren’t paid by year-end) and decrease taxable income in 2021 (as a result of increased deductions that were pushed into the following year).

Whether To Accelerate Income Into (And Defer Deductions Away From) 2020…

Ultimately, the potential for higher rates in 2021 is real, but exactly what the rate would be, and who would pay those rates, is far from certain. $400,000 is the proposed “line”, but it’s not clear how that would even be applied for individuals versus married couples. There has been discussion of repealing the Tax Cuts and Jobs Act (which would revert the top tax rate to 39.6%), but the Democrats have also suggested at various points in recent years the potential for an even higher top tax bracket. Not to mention the fact that a Presidential platform is just a candidate’s wish list. And while a President presiding over a Congress controlled entirely by his/her own party typically does have a substantial amount of political capital and influence over what proposed legislation will look like, ultimately, that legislation must be created by the legislative body, whose political and philosophical interests may not align precisely with the President’s agenda (which means even in the event that the Democrats gain control, it’s not clear that the Biden tax plan as proposed will precisely be the final legislation that’s enacted).

Thus, the decision to accelerate income for a taxpayer making $450,000 a year is dramatically different from the decision to accelerate income for the taxpayer making $1 million per year. In all likelihood, the latter will always be in the highest tax bracket (at least while they continue to earn a similar level of income), whereas the same is far less certain for the former.

That said, the potential ‘damage’ done via an increase in tax rates could be much more dramatic for individuals who are not already in the highest income tax bracket. More specifically, most Democrat-backed proposals call for an increase in the top tax rate to the pre-TCJA top rate of 39.6% (albeit with the potential that an even higher rate might be proposed at the top income levels – though, with an at-best-50-50 split in the Senate, Democrats are likely to be cautious of going ‘too far’ and risk losing the vote of even a single purple state Democrat, thereby derailing their entire package). That’s an increase of ‘just’ 2.6% over the current top 37% rate. By contrast, $400,000 of taxable income currently puts a married couple filing a joint return in the 32% bracket (which ends at $414,700). Thus, an increase in the rate applicable to the next dollar of income would be an increase of 7.6%, nearly 3 times the increase for those already in the top income tax bracket!

The end result is that while those with less than $400,000 of income aren’t even targeted by the proposal, for those above the prospective threshold, clients who are just slightly above the threshold may actually have the most to lose with potential tax bracket changes but also the most adverse impact if they accelerate significant amounts of income but no changes occur… while those significantly above the threshold have less potential benefit for accelerating income, but if they’re already in the top tax bracket, there’s limited downside to accelerating income even if tax brackets aren’t changed.

The (Limited) Impact Of A Potential Biden Increase In Long-Term Capital Gains Rates

While the Biden tax plan has proposed a potential increase in ordinary income tax brackets for those above $400,000 of income, when it comes to long-term capital gains the “good” news is that the threshold is higher – a $1M before higher capital gains tax rates would apply – but the consequences are also more severe, with the Biden proposal targeting excess long-term capital gains above the threshold to be taxed at ordinary income tax rates (which themselves may be higher if Biden is able to pass his proposals).

Nonetheless, the decision of what to do with long-term capital gains is likely straightforward for most taxpayers: if one is to believe that the Biden-platform income figure of $1 million is ‘real’ (and will remain in any final proposals if they do come to pass), the long-term capital gains rate is not likely to rise in 2021 for most taxpayers even if Biden is able to implement his tax plan. Thus, there is no need to accelerate the sale of investments not otherwise intended to be sold in 2020 into 2020.

For those with income in excess of $1 million, who thus may have capital gains that fall above the new threshold, the decision is significantly more nuanced. On one hand, the cost of selling such investments in 2020 (i.e., harvesting capital gains in the current tax year before the increase) would trigger a 20% long-term capital gains tax, plus a 3.8% Medicare surtax on Net Investment Income. That’s to say nothing of state and/or local taxes, which could bump the total tax bill to 30% or more. Voluntarily paying a tax bill of 30% today might be a tough pill to swallow for many high-income individuals, particularly on “long-term” investments that otherwise might not have been sold and could have continued to compound… even if it means paying a lower rate than they might otherwise face in the future.

Still, though, if the Biden proposal to ditch long-term capital gains rates in favor of ordinary income tax rates for those with income in excess of $1 million was to become law, it would nearly double the current top federal rate associated with such income from 20% (the top long-term capital gains rate), to 39.6% (the proposed future top ordinary income tax rate)! That might be an even-more-bitter pill to swallow. If so, perhaps paying the still-high-but-not-that-high taxes that would be owed if a sale of appreciated assets were to take place prior to the end of 2020 may be the best of bad options.

The end result is that while most households can likely proactively plan to not take action regarding their capital gains exposure – simply because their income isn’t currently and isn’t anticipated to be materially higher than $1M – for those who do face the possibility of being above such thresholds (either by already being high-income or the potential of having a very highly appreciated investment that may be sold in the coming years for sizable gains) the stakes are high to consider taking at least some of the gains off the table in the form of harvesting long-term capital gains before the end of this year.

Planning For Potential Elimination Of Step-Up In Basis And Capital Gains At Death

But, as if that decision wasn’t complicated enough on its own, further complexity is added to the mix when considering the additional Biden tax proposal calling for the elimination of the step-up in basis of capital assets upon death. As under current law, the appeal of not selling and triggering long-term capital gains is the potential to permanently avoid such capital gains by holding until death and receiving a step-up in basis. But in the future, taxpayers with large unrealized capital gains could find that holding all of their appreciated assets to be deemed sold at death could result in more than $1 million of capital gains income at that time, leading to a tax rate on some (or potentially even all) of the gain at the proposed 39.6% rate! Ironically, holding appreciated assets until death would rapidly switch from a very desirable tax strategy to an especially undesirable one (because taxing all appreciated investments at death, all at once, would be even more likely to push capital gains into the new higher capital gains rate!).

Furthermore, the Biden proposal does not call for any sort of exemption in the elimination of the step-up in basis at death. It’s hard to imagine, however, that such a change would take place. Rather, while there is no guarantee of this playing out, a more likely outcome is that in the elimination of the step-up in basis would look more like 2010, when the elimination of the estate tax was coupled with a limited step-up in basis of $1.3 million for non-spouse beneficiaries, and an additional $3 million of basis that could be allocated to property inherited by a surviving spouse.

Absent such an exemption amount, there would likely be an undue burden on taxpayers with more modest income from both a reporting and a practical perspective. For instance, many taxpayers' net worth is largely tied up in their home, a fairly illiquid asset that could present significant problems to heirs if it were treated as sold upon the death of the owner.

Example 1: Jack bought his home 40 years ago for $25,000, and over the years put in an additional $175,000 of capital improvements. Thus, his total basis is $200,000. In addition to Jack’s home, which is currently valued at $700,000, his only other asset is a $25,000 bank account.

If Jack dies and death is treated as a realization event, and there is no exemption to the no-step-up-in-basis Biden-proposed rule, Jack would have a capital gain of $525,000 on his final income tax return (or $275,000 if Jack’s heirs were able to utilize the $250,000 exclusion amount that applies to the gain of individuals who liquidate their primary residence). Between Federal and state income taxes, that could easily lead to an income tax bill of $80,000 or more (and more than $40,000, even after the application of the exclusion, should it apply).

What if Jack’s heirs, likely his children, don’t have enough money to pay that tax bill? Would Uncle Sam really force them to sell Jack’s house, the family residence for 40 years, in order to satisfy the death-caused income tax bill? It’s hard to imagine that scenario playing out in reality.

Plus, for those individuals with large unrealized gains, elimination of the step-up in basis and the treatment of death as a realization event doesn’t necessarily spell disaster from a tax perspective… provided they just live long enough to strategically sell their investments during life!

Example 2. Jill is the 60-year-old owner of a brokerage account that has $6 million in cumulative assets that have a cumulative basis of $2 million. Jill’s income typically hovers around $300,000 per year. Thus, her income is $700,000 below the Biden-proposed $1 million threshold above which long-term capital gains would be taxed as ordinary income.

If President-Elect Biden’s platform was to be enacted as proposed, and if Jill died, there would be a $4 million capital gain upon her death, of which the majority will be subject to ordinary income tax rate of 39.6% (plus the 3.8 % surtax).

Suppose, however, that Jill is in good health, and there is no reason to think that death is on the immediate horizon. Beginning in 2021 and continuing on until no longer necessary, Jill could begin harvesting $700,000 of capital gains each year without subjecting any of that amount to the Biden-proposed ordinary income tax rates. Thus, even with future anticipated growth factored in, within a decade, and by the time Jill was 70 years old, she will have been able to liquidate her investments and pay tax on the gain at a rate similar to the rate she would pay today.

Meanwhile, if at least one of the Senate seats in Georgia goes Republican, or Democrats simply don’t enact an elimination of the step-up in basis even with control, Jill (in the example above) is not forced to trigger a large tax bill today that would prove entirely unnecessary. Of course, those changes could occur, and Jill could have a heart attack at 61, rendering the sell-over-time plan effectively meaningless.

Harvesting Income To ‘Buy Tax Insurance’ Against 2021 Tax Legislation?

In the end, the decision to accelerate income into 2020 – whether it be ordinary income or long-term capital gains – is in large part a decision to ‘buy tax insurance.’ It represents a willingness to pay a price (current tax rates) today, that may or may not turn out to be a good deal, in exchange for a guarantee that minimizes additional cost.

Accordingly, since the political landscape for 2021 and beyond is still unknown, the decision to accelerate income into 2020 is as much a personal choice, that factors in a client’s own tolerance for potential future tax hikes, as it is a mathematically-based decision.

For some clients, the peace of mind that will come from a decision to accelerate income into 2020 will be worth the potential downside of paying income tax before it would otherwise be necessary to do so. Particularly for those who may already be subject to top tax brackets, which means there’s limited adverse impact to accelerating income if the Biden tax plan doesn’t pass (it was going to be taxed at top rates anyway?), but significant upside if the Democrats are victorious in the Georgia run-off and do obtain the necessary Senate control to enact new legislation.

On the other hand, for others who either doubt the likelihood of tax hikes occurring for 2021, or for whom the cost of buying the tax insurance (the additional tax costs resulting from the acceleration of income in 2021) is too much to stomach – especially if doing so would drive up their tax rates today by accelerating so much income – the wait-and-see-what-happens approach is likely to be more appealing.

End Of Year Planning By Deferring Income Tax Deductions?

With the potential for an increase in tax brackets in 2021 under the Biden tax plan, not only is there potential appeal to accelerate income into 2020 (at current tax rates before they increase), but there is also appeal to defer deductions into 2021 (to potentially claim them against higher future tax rates).

However, another key part of President-Elect Biden’s tax platform is a prospective “cap” on the maximum benefit of itemized deductions at “just” the 28% tax bracket. If such a cap were to be enacted as part of a Democrat-backed piece of tax legislation, the value of itemized deductions for high-income taxpayers might actually go down (because instead of the 33%, 35%, or 37% ‘break’ they receive today for such amounts, they will only receive a 28% ‘break’), even though their tax rate is increasing!

Which means those who are currently in higher tax brackets today would actually benefit more by claiming their deductions in 2020 at current rates, and not in 2021 at “higher” tax rates because those subject to higher future tax rates will also be subject to a 28% cap on their deductions!

Nerd Note:

In 2021, the 32% income tax bracket (the first income tax bracket for which the rate exceeds 28%) begins at a taxable income of $164,926 for single filers, $329,851 for married couples filing a joint return, and $164,901 for those filing as a head of household.

The end result is that while there may be appeal for some high-income taxpayers to accelerate ordinary income (and for very high-income households, capital gains as well) into 2020, in order to capture that income at current tax rates, it is decidedly not favorable for high-income households to defer deductions into 2021 that they could otherwise claim in 2020!

As in the end, if Republicans can hold on to at least one of the two Georgia Senate seats, it’s unlikely we’d see a cap on the benefit of an itemized deduction, but there won’t likely be an implementation of the Biden tax plan and higher tax rates in 2020, anyway. On the other hand, if Democrats take both Georgia Senate seats and control the Senate (along with the House and the Presidency), it becomes more likely that tax rates will rise, possibly as soon as 2021, but then the new 28% cap on itemized deductions is more likely as well. Either way, deferring deductions for high-income households into 2021 generally will not be favorable!

Deferring Deductions For ‘Everyone Else’ And The Potential Repeal Of The SALT Cap?

While in general, deferring deductions is not a favorable strategy – it’s better to claim a tax deduction sooner rather than later (if only to capture the time value of money), and higher-income households actually face the potential that their itemized deductions could be less valuable in the future – there are situations where households may want to consider deferring expenses that (may) qualify as itemized deductions. A prime example of such an expense would be state and local tax payments, from income (e.g., fourth-quarter estimate) taxes to property (e.g., real estate or automobile) taxes.

The reason is that under the Tax Cuts and Jobs Act, deductions for state and local taxes (“the SALT deduction”) are ‘capped’ at no more than $10,000 (for both single taxpayers and married couples filing a joint return). And unfortunately, the $10,000 cap includes both state and local income taxes, as well as property taxes. Given this fairly modest cap, many clients have already far exceeded their $10,000 maximum SALT deduction, and therefore, making additional SALT payments in 2020 will yield no additional tax benefits.

By contrast, making the same payments in early 2021 could lead to some sort of tax benefit if the SALT cap is repealed. Sure, there’s no guarantee that will happen, but do you know what is certain? That it won’t happen this year! So, why not push the expense out until 2021, when there’s at least a chance?

Nerd Note:

Perhaps surprisingly, repealing the cap on the SALT deduction was not actually a part of the formal Biden platform during the election. Nevertheless, Democrats, as a whole, have repeatedly cited it as a prime target for repeal. Thus, in the event that Democrats gain control of the Senate and attempt to pass significant tax reform, it is likely a repeal of the SALT cap would be included in such a bill.

The SALT cap, of course, is not the only reason a client may be unable to see a tax benefit for a 2020 expense that qualifies as an itemized deduction. The high standard deduction amount, itself, remains a barrier for many taxpayers. Notably, after the Tax Cuts and Jobs Act roughly doubled the standard deduction amounts, the number of taxpayers who itemize deductions on their Federal income tax return dropped from about one-third of taxpayers to about 10% of taxpayers (preliminary data for 2019 showed 9.6% of taxpayers itemized deductions on their Federal return). Thus, many clients, and sometimes even those with a high net worth and/or high income, continue to take the standard deduction.

Like the potential for a repeal of the SALT deduction limit, there is no guarantee that any Democratic tax bill would call for a reversion to previous standard deduction levels… but it’s possible. So, if you know your client won’t be able to receive a deduction for a charitable contribution, or a medical expense, etc. this year (2020), it makes sense – at least from a tax planning perspective – to push that expense off until January 2021.

In the end, this means that high-income taxpayers generally will not want to defer deductions into 2021 (and instead can/should claim whatever they can benefit from in 2020), while those who are not able to enjoy the full benefit of a potential itemized deduction – whether due to the SALT cap, or an inability to exceed the Standard Deduction threshold – may want to consider delaying whatever otherwise-deductible expenses they can into 2021, “just in case” a Biden tax plan adjusts deductions or thresholds in a manner that turns out favorable. It can’t be worse than getting no value for the deduction in 2020 anyway!?

Planning For The Possibility Of Reduced Estate And Gift Tax Exemptions

As part of the Tax Cuts and Jobs Act, the previous estate and gift tax exemption was doubled from an inflation-adjusted $5 million to $10 million. After accounting for inflation in the years since the estate and gift tax exemption for 2020 is $11.58 million. Accordingly, thanks to portability, married couples effectively have 2 × 11.58 million = $23.16 million of estate and gift tax protection under the current law.

At those thresholds, the overwhelming majority of advisors’ clients have little to nothing to worry about with respect to Federal transfer (estate and gift) taxes, with only a few thousand households in the entire country subject to Federal estate taxes at death each year now. In the event Democrats are able to ‘land’ both Georgia Senate seats, though, it is likely that they would seek to repeal the changes to the estate and gift tax exemption made by the Tax Cuts and Jobs Act, as was proposed as part of the Biden platform, returning the future exemption amount to approximately $5.85 million per person (what the original $5M exemption would have inflation-adjusted to by next year). Whether such changes would occur effective to the date of enactment, prospectively for 2022 in future years, or even retroactively to the beginning of 2021, is unclear.

While $5.85 million of estate and gift tax protection per person ($11.7 million of protection for a married couple) is still more than enough to prevent not only most taxpayers but also most advisors’ clients (who tend to have higher net worth than the ‘average’ taxpayer) from ever having to deal with Federal transfer tax issues, such a decrease in the exemption would obviously result in a substantial increase in the number of taxable estates.

Notably, given the current state and gift tax rate of 40%, the loss of a combined $11.7 million of protection for a married couple could create an additional $11.7 million x 40% = $4.68 million an additional estate tax liability. That’s not chump change!

With that in mind, many high-net-worth individuals are contemplating using some or all of their current (high) exemption amount before it is potentially lost. This is especially true since the IRS provided guidance that in the event of a future reduction in the estate and gift tax exemption, transfers today in excess of the future exemption amount will not be subject to any clawback.

Who Should Plan Around A Potential Reduction In Estate Tax Exemptions?

In addressing the potential changes to the estate and gift tax exemption with clients, there are really three distinct groups of individuals to consider: those who almost certainly will not have to deal with transfer tax issues, those who almost certainly will have to do with transfer tax issues, and households who may or may not have to deal with transfer tax issues depending upon growth of assets, life expectancy, and/or whether changes to lower the gift and estate tax exemption are enacted.

If clients fall into the first group of taxpayers, who don’t really need to worry about transfer tax issues, accelerating otherwise unplanned gifting into the end of 2020 is largely unnecessary. At the opposite end of the spectrum, for those taxpayers with a net worth that will almost certainly subject their estate to an estate tax liability upon their passing, there is a strong impetus to act now, to ensure they do not lose out on maximizing the current exemption amount. Nevertheless, for some the decision may still present a bit of a challenge.

For instance, a single, ‘ultra-mega-high-net-worth client’, with a net worth of $100 million or more, is likely to be much more amenable to utilizing their full gift tax exemption (of $11.58M) in 2020 than would a similar individual with a net worth of $14 million. First, the individual with a net worth of $100 million is likely just fine from a lifestyle perspective living on only ~$88 million going forward. By contrast, the individual with a $14 million net worth would have ‘just’ ~$2 million left after utilizing their full gift tax exemption amount.

Furthermore, a substantial portion of many high-net-worth taxpayers’ estate is comprised of the ownership of business assets. Individuals with ultra-mega-high-net-worth are likely to be able to gift an amount equal to the current exemption to an irrevocable trust, or to other heirs, while still maintaining control of the business. By contrast, individuals with smaller, but still potentially taxable estates (e.g., those with $15M+ of net worth), may not have the same luxury of transferring business shares while maintaining business control, which could be a dealbreaker for many.

For individuals whose taxable estate ‘fate’ is less certain – i.e., those who have “just” $5M to $10M of net worth and may or may not be above or below a future exemption depending on their growth, spending, availability of portability, etc. – the decision of what to do now is much more complicated. On one hand, such individuals are not likely to want to see millions of dollars lost to Uncle Sam in the form of estate taxes if the exemption amount is materially lowered in the future. On the other hand, the same individuals are likely to be fairly resistant to gifting substantial portions of their assets now, because they are more likely to need them (or at least want to have them readily available to use).

For instance, consider the case of a single individual with a net worth of $10 million. Under the current rules, the individual would not have any Federal estate tax liability upon their death. If, however, the exemption amount is reduced as proposed in the Biden platform, the change would result in the creation of a roughly $1.6 million tax bill upon the individual’s death (40% of the excess above $5.85M)! The same would be true for a married couple with a $16M estate.

In order to avoid such a fate on a guaranteed basis, though, the individual would have to give away their entire net worth now.

Example #3. Peter has a net worth of $10 million. He feels that he needs $2 million to live on for the remainder of his lifetime, and would like to try to avoid all transfer taxes. Unfortunately, his two goals are not really compatible.

Could Peter give away ‘just’ $8 million, leaving himself $2 million dollars to live on for the balance of his life, and using what is anticipated to be a $6+ million future exemption to cover his $2 million remaining net worth? Unfortunately, if he dies with that $2 million still in his name and after a reversion to the pre-TCJA estate and gift tax exemption levels, the $2 million would be subject to Federal estate taxes, creating an $800,000 Federal estate tax bill!

The reason is that the formula to determine how much estate or gift tax exemption a person has remaining (for gifts during life or to avoid estate taxes upon death) is essentially equal to the following formula: Current statutory exemption amount – previous gifts = remaining available exemption. To the extent the remaining available exemption amount is a positive number, that’s the amount that can be used to effectuate additional transfer-tax-free transfers of wealth. If the number is $0 or less, transfer taxes will apply to future transfers.

Thus, if Peter dies having given away $8 million and with $2 million of remaining assets at a time when the current estate tax exemption is (hypothetically) $6.5 million, his remaining exemption amount at death is $6.5 million - $8 million = negative $1.5 million… or stated more simply, he won’t have any remaining exemption left, such that his $2 million of remaining assets are still fully subject to estate taxes!

Or viewed another way, Peter’s gift may have occurred previously when the exemption amount was higher, but his prior gifts are counted against his current exemption in the future. Which in a world of rising estate tax exemptions was simply a straightforward way to ensure that prior gifts filled up the earlier estate tax exemption (and a new higher exemption stacked on top). But in the event that the estate tax exemption is reduced, Peter’s prior gifts that only used part of the earlier higher exemption amount can end out completely using his reduced future exemption amount!

Notably, the end result when the estate tax exemption is reduced is that the IRS’s anti-clawback position means that the IRS won’t retroactively impose transfer taxes on the additional $1.5 million Peter was able to transfer out of his estate without estate/gift taxes by virtue of making a gift in 2020, when the exemption was higher, as opposed to bequeathing the assets at his death. But there is no remaining exemption amount to ‘absorb’ the last $2 million remaining in Peter’s estate upon his death. Accordingly, again, the entire amount will be taxable, creating a $2 million x 40% = $800,000 estate tax liability.

Consequently, taxpayers in situations like Peter’s are stuck between the proverbial rock and a hard place: leave themselves penniless – because they must utilize the entire current estate tax exemption to fully benefit – or risk the imposition of future estate/gift taxes if the exemption amount is lowered.

End-Of-Year Estate Planning Strategies For A Potential Change In Estate Tax Exemption

While the decision-making process for end-of-year estate planning is going to be tough for many clients, there are some potential opportunities for advisors to suggest planning strategies that can help ‘split the difference’, including:

- The use of Spousal Lifetime Access Trusts (SLATs) by married couples. Such trusts can allow an individual to utilize their full gift/estate tax exemption while retaining some access to the funds via their spouse. It’s not a perfect solution, however, as death of the spouse or divorce can substantially complicate matters.

- Using one spouse’s full available exemption before using any of the other spouse’s exemption. In many cases, couples like to do things together, but when it comes to gifting assets out of their estate, that’s likely not a great idea.

For instance, suppose an older couple with $16.58 million is comfortable living on ‘just’ $5 million. In order to avoid future potential transfer taxes, the couple may be willing to gift $11.58 million out of their name today (but retain the remaining $5 million to live on). If the couple splits this amount, with each spouse giving just over $5.75 million away, and the exemption amount is halved by Democrat-led legislation next year, the couple, as a whole, will have little to no remaining estate tax exemption left, as both spouses would have used a $5 million inflation-adjusted exemption amount already (in a manner similar to what happened to Peter in Example #3).

By contrast, if just one of the spouses use their full $11.58 million gift tax exemption in 2020, and the same reduction to the gift and estate tax were to occur in 2021, the other spouse would continue to have their $5 million inflation-adjusted exemption left! Thus, the couple’s remaining assets could pass free of Federal estate tax upon that spouse’s death by using all of one spouse’s exemption but not half of each!

- Preparing the client to use non-exemption-using strategies in the future. For clients with no gift and estate tax exemption left in future years, or whose estates will likely exceed their available exemption at the time of their death, renewed attention should be given to planning strategies that can reduce the overall estate and/or gift tax bite, without utilizing further exemption amounts. Such strategies include not only proactive use of the annual gift tax exemption amount (though its possible other changes could curtail this strategy as well), but also the use of Grantor Retain Annuity Trusts (GRATs), Private Annuities, and sales to Intentionally Effective Grantor Trusts (IDGTs). With the caveat that there is still some risk that these strategies, too, are subject to new limitations under a Biden tax plan, which has not been explicitly proposed in Biden’s current plan but was a part of prior Democrat tax proposals under President Obama and Vice-President Biden.

The November 3, 2020 elections produced a wholly unsatisfying result for financial advisors and their clients from a financial planning perspective, regardless of their political affiliation. The political clarity, leading to planning clarity, that many had hoped for, did not emerge. Instead, the planning community must collectively hold its breath until early January 2021 to see what the political landscape, and the likely potential tax policies to follow, will look like for the next few years.

In the event that Democrats take both seats in the Georgia runoff elections to fill its U.S. Senate seats, it’s likely that Democrats would swiftly move a follow-up COVID-19 relief bill through the legislative process, but after that, changes to the Internal Revenue Code and to healthcare legislation would be among the top priorities.

By contrast, If Republicans are able to hold on to at least one of Georgia’s U.S. Senate seats, it creates a near-certainty that major changes to the Internal Revenue Code won’t be happening for at least the next two years (until the balance of power in the Senate will once again be up for grabs). If such a scenario comes to fruition, though, it could lead to Republicans and Democrats working together on areas of common ground… relatively speaking, of course. Such areas include at least ‘minor’ tax law changes that might be attached as part of a compromise in future COVID-related economic stimulus, or the potential for an (even more) expanded child tax credit and further retirement-related changes.

Ultimately, the key point is that now that the election has passed, clients are looking for guidance as to what they should be doing – or not doing – before the end of 2020 and beyond. And while in many cases, the ‘right’ answer may not be able to be definitively known today, and in other situations the best move may actually be to ‘do nothing’ (as the scope of proposed changes is still fairly limited to a subset of very high income and high net worth households, even above the threshold of who many financial advisors serve), not having the conversation at all is decidedly the wrong ‘move’ for proactive advisors seeking to reassure and inform clients.

Does a first proposal ever become tax law? There is a House plan, a Senate plan, a committee to reconcile the two plans into a bill, etc etc. I don’t think we will know the particulars until much later in the process. Until then it’s just speculation.

You are in safe hands

CREDIBLE tax services & RAPID REFUND

We have a reputation for good, speedy tax services.

Whether you are filing for the first time with a simple tax return or

have had difficult experiences with filing for your tax. The U.S.A tax

services will work with you to ensure that you get super sized tax

returns. Whatever the situation you have with filing for tax we say “bring it on”. If you want to speak with one of our agents, you can click HERE>>https://www.theusataxservices.com/Home/Services#contact