After several years of speculation and more than a year since the President issued an Executive Order on “Strengthening Retirement Security in America”, the IRS has released its proposal to update the life expectancy tables used to calculate the annual Required Minimum Distributions (RMDs) from all sorts of tax-preferenced accounts, including IRAs and 401(k)s, for both lifetime account owners and their (stretch) beneficiaries. Most notably, this is the first time the tables have been updated since 2002, despite the fact that life expectancy has increased more than 2% (or 1.6 years) for all Americans, and more than 8% for Americans who have reached the age of 65!

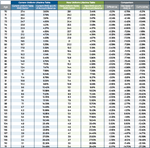

Central to the proposal (which must still go through the formal approval process and thus might not “go live” until sometime next year, though the proposed changes wouldn’t take effect until 2021 anyway) are updates to the RMD factors used to calculate required minimum distributions themselves in each of the three different life expectancy tables, including the Uniform Lifetime Table (for retirement account owners to calculate their RMDs during their lives), the Joint Life And Last Survivor Expectancy Table (used by account owners who have named a spousal beneficiary who is more than 10 years younger), and the Single Life Expectancy Table (which is used by beneficiaries of inherited retirement accounts to calculate their so-called “stretch” distributions).

However, while lowering RMDs across the board will result in some increased tax deferral benefits, the changes likely won’t have as much of an impact for retirement account owners and beneficiaries as was likely hoped for. Specifically, according to data provided by the IRS, of the Americans who are required to take distributions from retirement accounts, only roughly 20% are taking no more than the minimum required. Which means that the remaining 80% are taking more than the required minimum, thus making any decreases in RMDs a moot point.

The question then becomes, will lowering RMDs for those 20% (who likely already have enough wealth to meet their retirement needs in the first place) have a material impact on their account balances as they age? For account owners and beneficiaries who have been extremely fortunate with their returns over the years and have much-larger-than-typical account balances, perhaps. However, when considering someone with an IRA valued at $1 million, the first year RMD would only decrease by roughly $2,100, and only a portion of that amount would have been due as taxes; the value of deferring that tax liability is only the growth potential on those taxes… which are hardly amounts that could significantly alter someone’s overall financial picture later in life (especially for already-affluent retirees), even when considering that the RMD factors continue to increase through the years.

And that lack of impact stretches even to those who have much longer life expectancies, such as younger individuals who have inherited a retirement account and use the Single Life Expectancy Table. A 40-year-old, for example, would see only a tenth of a percentage point decrease in the required distribution amount in the first year, which won’t be a very material difference, even for those who rely on that extra income from an inherited retirement account.

Notably, though, individuals taking RMDs will need to consider the transition to the new life expectancy tables if/when they take effect in 2021. Which, for lifetime RMDs for existing retirement account owners, is fairly straightforward – to simply use the new table in 2021 – though those who defer their first age 70 ½ RMD from 2020 into 2021 must still use the ‘old’ tables for the 2020 RMD. In the case of beneficiaries of inherited retirement accounts looking to stretch, the transition process is a bit more confusing, as such beneficiaries cannot simply use the new life expectancy tables going forward at their current age. Instead, they must retroactively determine what their ‘original’ stretch period would have been in the past under the new tables, and then adjust forward to where that distribution schedule would be today (by subtracting 1 for each subsequent year since the year after the original account owner’s death).

Ultimately, the key point is that, while updates to the life expectancy tables have been a long time coming (especially since other tables – like those used by the IRS to analyze life insurance contracts – have already been updated to reflect longer lifespans years ago), the proposed changes simply won’t make much of a difference for the vast majority of retirement account holders and beneficiaries. Still, for those who take ‘only’ the minimum required by the IRS, the decreases might not provide that much of a benefit, but at least it does help to defer some taxes, which is hardly ever bad news.

Welcome back to the 150th episode of Financial Advisor Success Podcast!

Welcome back to the 150th episode of Financial Advisor Success Podcast!