For financial advisors, the new Qualified Business Income (QBI) deduction (also known as the IRC Section 199A deduction, or the pass-through deduction) presents not just many tax planning opportunities for small business owner clients, but also tax planning opportunities for financial advisors themselves as small business owners. The caveat, however, is that the 20% QBI deduction may be very limited for financial advisors, because they are classified as "Specified Service Business" owners under the new rules, and, as a result, any "high income" advisors (defined as those whose taxable income exceeds $315,000 when filing a joint return, or $157,500 when filing otherwise) are subject to a phaseout of their potential full QBI deduction.

In this guest post, Jeffrey Levine of BluePrint Wealth Alliance, and our Director of Advisor Education for Kitces.com, examines how high-income financial advisors (and other Specified Service Businesses) can utilize strategies to get the most benefit from their QBI deduction, including spinning off and renting back depreciable property, creating a PEO and leasing back employees, condensing lifetime giving via the use of a donor-advised fund, and other strategies!

The good news of the new QBI rules, and the phaseout for Specified Service Businesses (including financial advisors), is that it still takes a fairly substantial income to phase out the deduction, and for those under the income thresholds, the full QBI deduction remains available. On the other hand, because the QBI deduction phaseout is based on total household income from all sources (albeit after all deductions), even advisors who themselves don't earn more than the threshold amount may still end out phasing out some or all of the deduction based on other income (e.g., spousal income, real estate income, portfolio income, etc.).

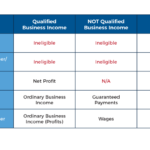

Fortunately, though, not all is lost for financial advisors who have entered into the QBI phaseout zone. First and foremost, advisors can look to strategies that convert the advisor’s specified service business income into "other" income derived from a non-specified trade or service business, such as by spinning off any firm-owned real estate into a separate entity (and leasing it back at fair market value), spinning off non-advisory employees and leasing them back through a professional employer organization (PEO) (as a PEO would be eligible for a QBI deduction, so long as it is not deemed an advisory business), or holding the firm's intellectual property under a different entity and then licensing it back to the firm (as the intellectual property income may be eligible for a QBI deduction). The net result of such strategies is that the advisor's total income is the same, but occurs by reducing the amount of specified service business QBI generated from their practice (as rent, employee leasing, etc, are deductible business expenses), while simultaneously increasing the amount of QBI generated from the separate (non-specified-service and QBI-deduction-eligible) businesses.

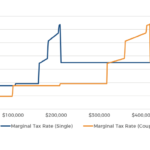

For those who are in the midst of the QBI phaseout zone, planning can be even more impactful, as marginal tax rates during the QBI phaseout can spike as high as 64%... which may lead advisors to increase investment into the firm (as deductions are more valuable at the higher rate!), shift income to other years (that are outside the phaseout zone), or potentially even cut back on their workload (if they're really only keeping 36 cents on the dollar before the additional impact of state income taxes!).

Ultimately, the key point is to acknowledge that high-income financial advisors (and other specified service business owners) have considerable opportunity to plan around the new QBI phaseout zone... even if their total income is within or well beyond the QBI phaseout zone! While the new rules can be a bit tricky (and strategies could shift as the IRS provides more guidance going forward), it appears that QBI strategies will be a key focus going forward, and present a considerable planning opportunity for advisors (and their clients!) to reduce their overall tax burden!

Welcome, everyone! Welcome to the 78th episode of the Financial Advisor Success Podcast!

Welcome, everyone! Welcome to the 78th episode of the Financial Advisor Success Podcast!