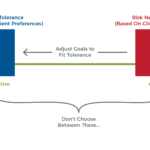

For prospective retirees who don’t simply want to annuitize most or all of their wealth, determining how best to invest a retirement portfolio to generate income is a substantial challenge. Not only because of the need to invest for enough growth to sustain inflation-adjusting retirement distributions over time, and managing portfolio volatility to avoid triggering an adverse sequence of returns in the first place… but also because, as retirement investing has evolved beyond simple strategies like “buy the bonds and spend the coupons” and into more total return strategies, it’s surprisingly difficult to come up with a system to actually generate the distributions themselves.

After all, most prospective retirees who are looking at making the transition away from work have spent the better part of 40 years paying their ongoing bills from a steady series of monthly or perhaps bi-weekly paychecks. Which means the most straightforward way to facilitate retirement is simply to re-create those ongoing retirement paychecks. Except as noted, modern retirement portfolios – especially those that include both income and growth (i.e., capital gains) components – aren’t necessarily conducive to generating consistent retirement paychecks. At least not without creating a system behind the scenes to ensure the cash will be there as needed.

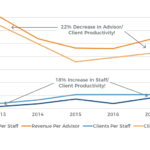

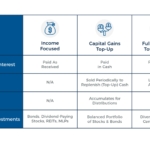

Over the years, advisors have created a number of different systematic approaches to address the retirement paychecks challenge. For some, it’s about investing into a “traditional” income-generating portfolio of bonds and dividend-paying stocks (perhaps supplemented today by income-generating alternatives like REITs and MLPs), and simply passing through the income as received. For others, it may start with accumulating interest and dividends, but then “topping up” the portfolio’s cash with periodic liquidations of capital gains. For still others, with the ongoing decline of transaction costs, the approach has shifted to simply keeping all cash fully invested, and making liquidations as needed in real-time to generate retirement distributions without any cash drag at all!

Whatever the particular methodology, though, any advisor needs to be able to answer a number of important questions about their mechanical process of generating retirement paychecks, including how they will handle dividends and interest, whether there will be a cash position (or not), how capital gains liquidations will be handled (in various up- and down-market scenarios), the frequency of distributions (monthly, quarterly, or annual?), the sources of distributions from various account types, and how those distributions will be coordinated with the rest of the client’s retirement income picture (from Social Security to pensions and annuities to reverse mortgages).

The bottom line, though, is simply to recognize that the mechanical challenge of how to actually generate those retirement “paychecks” that transitioning retirees are accustomed to, is an entirely separate matter from just investing the retirement portfolio itself, and entails a number of distinct policy-based decisions about how to standardize a process for a wide range of retirees. In turn, advisors might even consider creating Withdrawal Policy Statements to then codify the processes they will use to generate retirement income withdrawals, just as an Investment Policy Statement is used to codify the processes used to invest the retirement portfolio itself!

Welcome back to the 96th episode of the Financial Advisor Success podcast!

Welcome back to the 96th episode of the Financial Advisor Success podcast!