The media provides no shortage of articles giving recommendations of how much households should save to afford retirement, from rules of thumb like “save 10% to 15% of your annual income” to more detailed research studies providing "precise" savings guidelines based on age, income level, and targeted retirement income replacement rates. The caveat to all of these tools, though, is that they presume the household has flexible discretionary dollars available to save in the first place.

Yet in reality, most households struggle to save because there is no money left at the end of the month to save in the first place. Because technically their problem isn’t a savings rate that’s too low; it’s a spending rate that’s too high, in one or more categories, that is causing all of the available household income to be consumed before the end of the month is even reached!

And sadly, there is remarkably little guidance available to households about what a prudent spending rate should be in the first place. In some of the largest categories, which tend to be financed with debt – e.g., homes and automobiles – lender guidelines place some restriction on the maximum amount of spending in each of those key categories. With the caveat that lenders don’t lend based on what is prudent for the borrower, but what will result in a permissible level of defaults and losses for the lender. Or stated more simply, borrowing guidelines are based on what the lender believes will extract the maximal amount of interest with an acceptable level of defaults… despite the fact that many of those borrowers will be in over their heads and struggling just to make their repayments!

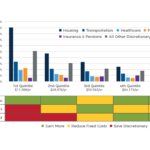

A somewhat better data set for households to evaluate the prudence of their spending comes from comparing an individual’s spending to the Consumer Expenditure Survey from the Bureau of Labor Statistics, which details what households spend in various categories, segmented by income level (as fixed expenses not surprisingly consume far more of a lower-income household’s budget than those with higher income levels).

Of course, comparing one’s spending by category to average spending rates (by income level) still doesn’t necessarily reveal what is prudent and what a household should spend, especially when recognizing that the national savings rate is already a dismally low 3.2% (which means comparing to CES data in the end simply compares to a national set of households that already are spending “too much” and not saving enough!).

Nonetheless, focusing on spending rates at least puts the focus back on what households can control – what they spend, and what they earn – rather than focusing on or criticizing a savings rate that ultimately is more a result of other decisions than a decision unto itself. And also helps to recognize that, for most middle-income households where spending is challenging, it is actually far better to focus on housing and transportation costs than trying to trim vacations, clothing, lattes and avocado toast from the budget.

But the question still remains: what is a prudent spending rate for typical household expenses, and how do you figure out what is or is not an appropriate amount to spend in the first place (that “lives within your means” and leaves an available dollar amount of savings left over)?

Welcome back to the 88th episode of the Financial Advisor Success podcast!

Welcome back to the 88th episode of the Financial Advisor Success podcast!