While there are an ever-growing number of advisory firms operating on the AUM model and offering “wealth management” services, there is still a significant gap between those that are ultimately still investment-centric, and the firms that are truly focused on financial planning first.

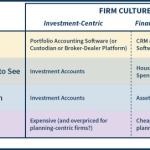

The significance of this difference in the culture of an advisory firm is that it impacts not only the depth of its investment vs financial planning services, but that it also shapes the technology decisions of the firm. Because the investment-centric firm is typically built around its portfolio accounting software as its core, while the financial-planning-centric firm uses its financial planning and CRM software as the hub of the business.

Yet despite the substantively different technology needs of the two firms, the overwhelming majority of advisor technology is still being developed for investment-centric firms, with at best only a token nod towards financial planning goals – even though, ironically, the financial-planning-centric software solutions often command a premium price in the marketplace!

Nonetheless, as the commoditization of investment management continues to drive more firms towards offering comprehensive financial planning services, the technology shift is beginning, from the rise of Turnkey Financial Planning Platform (TFPP) technology solutions, to the rising demand of planning-centric firms for a more financial-planning-centric client experience. Will advisor technology solutions step up to fill the void?