The Investment Policy Statement (IPS) is a staple of investment management and provides crucial guidance for (discretionary) investment managers about how to implement portfolio strategies on behalf of a client in times of uncertainty (when the client may not be there in person to help make the decision).

Yet the reality is that the concept of a “policy statement” transcends just the world of investments. Arguably, it can be effective across most domains of financial planning – not necessarily to establish a plan of action for the advisor in the absence of the client, but for the client today to establish a plan of action for handling an uncertain future. In this context, the “financial planning policy statement” is a form of choice architecture, narrowing future decisions in a manner that can help to eliminate the “bad” emotional choices from consideration.

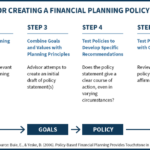

Of course, it’s still necessary to establish appropriate financial planning policy statements in the first place, linking underlying client values and core beliefs to structured policies that are flexible enough to address future unknowns, yet specific enough to provide clear, actionable guidance when the time comes. Which means the financial planner needs both a means to discover and understand a client’s values and beliefs (not just the financial data), and the tools to formulate and test policies that might be recommended to the client.

Overall, though, this kind of “policy-based financial planning” approach actually has the potential to provide the crucial link between financial life planning and technical financial planning strategies, serving as a means to translate values and beliefs into structured policy statements that can be implemented with the client. At least, if financial planning software is ever improved to the point that such financial planning decision rules can be illustrated in the first place!