One of the virtues of cash value life insurance is that insurance companies are willing to make loans against the policy at relatively favorable interest rates, because the insurance company knows that it can always foreclose on the policy (i.e., force its surrender) as collateral to repay the loan.

Unfortunately, though, while the availability of a life insurance policy’s cash value ensures that the loan will never be “underwater” with recourse to the borrower, the bad news is that the surrender of the life insurance policy itself can still be fully taxable for a substantial gain. Even if the policyowner doesn’t get any of the proceeds, because they’re used to repay the loan. Ultimately, the only way the upside of a life insurance policy becomes fully tax-free is if it matures as a death benefit.

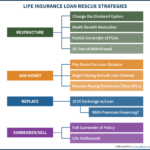

In fact, the reality that the only way to use a life insurance policy’s cash value to repay a loan tax-free is via the death benefit leads to a number of “rescue” strategies for life insurance policies with substantial loans, specifically to help ensure that the policy remains in place until the death of the insured.

In some cases, the accrued loan interest on a life insurance policy is so severe that there’s no way to save the situation – necessitating either a surrender of the policy, or perhaps a life settlement sale transaction for an older insured.

But fortunately, it’s often feasible to sustain the policy with some combination of restructuring the policy’s dividends and death benefit, engaging in partial surrenders or withdrawals, contributing some additional dollars into the policy (either as premiums, or to pay loan interest or repay principal), or even exchanging to a new “life insurance rescue policy” that transfers the policy’s cash value – along with the loan itself – in a tax-free 1035 exchange.

Of course, ideally the insurance policy will be monitored all along, to avoid ever reaching a “surprise” situation where a life insurance policy loan has compounded to the point that it needs to be rescued. But whether it’s a proactive “Bank on Yourself” borrowing strategy, or just accidentally accruing a loan through the Automatic Premium Loan provision on a whole life policy, sometimes a substantial loan does accrue, and it’s necessary to take steps to rescue the policy before an adverse tax consequence results!