Enjoy the current installment of "weekend reading for financial planners" - this week's edition kicks off with the huge news that Merrill Lynch is fully pivoting its retirement advisors to become level fee fiduciaries, eschewing commission-based retirement accounts entirely by April of 2017, and redirecting self-directed investors who still wish to trade to its Merrill Edge online brokerage platform or a new "robo" platform called Merrill Edge Guided Investing (though notably Merrill Lynch taxable brokerage accounts may still remain commission-based and are not subject to the new fiduciary rules). Also in the news this week was a decision from the DC Court of Appeals that has made a final ruling in favor of the CFP Board over the Camardas, which should end the ongoing lawsuit once and for all... and with the CFP Board's recent change to require mandatory arbitration, will likely be the last dispute any CFP certificant ever has with the organization that sees the inside of a courtroom.

From there, we have a few practice management articles specifically on the topic of hiring and retention, including: tips for hiring and retaining Millennial advisors; how to find the "right" team members by focusing first on cultural fit and passion (as long as the minimum technical skills are there); the importance of managing expectations for new employees to retain them going forward; and how "client-centric" firms aiming for high retention may be too client-centric, driving away their best employees (and ultimately damaging the firm's retention) in the process.

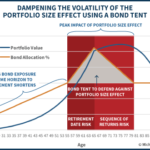

We also have several more technical articles, from a look at how to set "retirement guardrails" to determine when retirees may be spending too much (due to higher spending or poor market returns), to a discussion of how the community property rules interact with retirement accounts (and how a spouse's community property interest doesn't automatically ensure he/she can do a spousal rollover after death!), and an overview of how to use the IRS' Data Retrieval Tool (DRT) now that the 2017 FAFSA season is open.

We wrap up with three interesting articles: the first is a call-to-action for younger planners that despite being the "next generation" of financial planners, the time to lead is now (allowing for more time to build a foundation and enjoy the fruits of their labor!); the second is a look at the idea of practicing "radical generosity", giving especially deep and thoughtful gifts to clients, prospects, and referral sources, as a way to enhance the relationship; and the last is a look at how despite all the ongoing technological progress, the next 20 years may actually be far less disruptive than the past decades have been, as even "innovative" technology in recent years has actually been more incremental than truly revolutionary, and could actually drive consumers even more towards health care, education, and financial advising sectors, that remain uniquely human in their needs.

Enjoy the "light" reading!