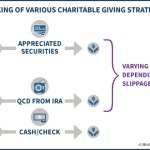

For those who already have a charitable intent and are over age 70 ½, the now-permanent rules permitted a Qualified Charitable Distribution (QCD) directly from an IRA to a charity provide an appealing means to minimize the tax bite of an RMD. Of course, it’s always possible to simply donate to charity and claim a charitable deduction to offset the income of an RMD, but given that in practice the income and deduction rarely offset each other perfectly, the QCD offers a slightly better potential tax outcome.

However, while donating from an IRA to satisfy an RMD obligation may be more effective than separately taking the RMD and donating cash (or writing a check) to the charity, it is usually not as good as donating low-basis stock or other appreciated investments instead. The reason is that while a QCD is a “perfect” pre-tax contribution, donating investments allows for a pre-tax contribution that also permanently avoids a long-term capital gain.

On the other hand, the reality is that charitable donations often have limits of their own, from the fact that they’re only valuable for those who itemize deductions in the first place, to the 30%- and 50%-of-AGI charitable contribution limits that may apply as well. Furthermore, donating low-basis stock may still not fully offset the income from an RMD, where that income increased AGI and triggered the phase-in of Social Security taxation or the phase-out of other significant deductions.

Ultimately, then, the relative benefits of QCDs will depend significantly on the facts and circumstances of the situation, driven primarily by whether or how much a donation of low-basis investments could really be claimed as a full deduction in the first place. On the other hand, it’s also important to remember that for those who don’t have a charitable intent in the first place, the optimal strategy is still to just take the RMD, pay the taxes, and keep the remainder; QCD strategies are still only best for those who want to maximize the tax benefits of charitable giving they already planned to do in the first place!