Financial planning is focused heavily on establishing and working towards very big long-term goals, from saving for a child’s education to accumulating the assets to fund a multi-decade retirement.

Yet the fundamental problem of “big” goals – financial planning or otherwise – is that they can seem so big and overwhelming that it’s actually demotivating. In the extreme, the goal may feel so distant and unachievable that it simply leads the person to give up on pursuing the goal at all!

Accordingly, the reality is that to really make long-term financial planning goals achievable, the key is to break them down into smaller pieces first. As the saying goes, the way to eat an elephant is one bite at a time. And the research of behavior change and motivation is increasingly finding that the “small wins” of successfully achieving small goals may actually be the key to helping us rewire our brains to stick with the new behavior in the long-run!

Unfortunately, though, financial planning education provides little in the way of training on how to break down big goals into small ones, and most financial planning software does a poor job of helping clients to track short-term goals!

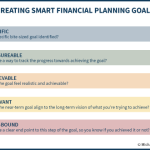

Nonetheless, in the world where the actual implementation of goals – i.e., into saving and investment accounts – is becoming increasingly commoditized, arguably it will be the process of helping clients break down big financial planning goals into smaller SMART goals that are Specific, Measurable, Achievable, Relevant, and Time-bound, and then providing them the tools to track progress and serving as an accountability partner to ensure follow-through, that may be the greatest financial planning value-add of all!

Read More...