Request a New Password Link

Fear of judgment is an emotion that creates anxiety for many people. For example, seeing a doctor can be stressful for people who fear they will be judged for the current state of their health (or for their health choices and behaviors). This anxiety can lead people to avoid going to a doctor altogether, even when they know that going would be the ‘right’ choice for the sake of their own health. Consumer research has suggested that this fear of judgment also extends to people who may benefit from hiring a financial advisor. Because just as it is common to feel anxiety about revealing the details of one’s physical health to a health professional, disclosing details about one’s financial health – and the potential for being judged based on their lack of financial knowledge or their past financial behaviors – can lead to Financial Advisor Anxiety (FAA).

While FAA can affect different people in different ways (for example, women were shown to feel more anxiety about being unfamiliar with financial terminology, while men worried more about being judged on their past behavior), the result often ends out being that people tend to avoid seeking out professional financial advice when their level of anxiety becomes too great.

For financial advisors, then, this means that a possibly significant number of potential clients may never even reach out… not because they don’t want or need financial advice, but because they are simply too anxious about the idea of revealing personal financial details to a stranger to take the step of making an initial phone call or email. However, advisors can help alleviate the impact of FAA on prospective clients – thereby improving the probability of potential clients actually reaching out to the advisor – by taking proactive steps to alleviate the fear of judgment before the initial contact.

For example, because unfamiliarity with financial terminology is a source of FAA for many people, adding a glossary of common financial terms (e.g., IRA, 529 Plan, Fiduciary, etc.) on the advisor’s website can be a helpful resource – not just as an educational tool, but also an acknowledgment that financial jargon can be obscure and intimidating to non-experts, and a signal that the advisor will not judge anyone for being unfamiliar with financial planning terminology.

Advisors can also alleviate FAA by sharing some of their own vulnerabilities by talking about their fears and challenges with finance. For instance, an advisor could record a video for their website about their own journey towards becoming an advisor, the obstacles they encountered in getting there, and the benefits they have realized by working to overcome their own anxiety. And in their own communities, advisors can model non-judgmental behavior to normalize some of the fear and stress that people often have when talking about money by, for example, talking openly in casual conversation about common financial issues that people experience (and how the advisor works with their clients to overcome them).

Ultimately, alleviating Financial Advisor Anxiety comes down to reducing the fear of judgment and shame that can paralyze some people into not seeking financial advice. And finding strategies to help individuals overcome FAA can be a powerful way for advisors to increase the number of prospects who reach out to them (because they were able to overcome their anxiety enough to do so). Which means that those prospective clients who do reach out will also be more likely to have a higher level of comfort and trust in the advisor from the start!

Welcome back to the 260th episode of the Financial Advisor Success Podcast!

Welcome back to the 260th episode of the Financial Advisor Success Podcast!

My guest on today's podcast is David Ortiz. David is the founder of Financial Chef, an independent RIA operating as a lifestyle practice, serving clients in southern Florida. What's unique about David, though, is the way he combines his experience as a classically trained chef with the growth of his advisory firm, which now includes driving a Sprinter van with a full kitchen, so he can travel to a wider range of clientele across South Florida, to cook custom meals for them and then provide financial advice while they eat their freshly prepared food together.

In this episode, we talk in-depth about how David grew his advisory firm by leveraging his training as a chef, first by building relationships with local charities, where he would provide in-house cooking for a party of 10 as a silent auction offering to get access to high-value prospects who are affluent enough to bid thousands of dollars on his donated chef services, how David then built an office space with a professional kitchen where the timing of client meetings was based on the available breakfast, lunch, and dinner sittings that restaurants use, and why David ultimately decided to make his cooking plus advice services more mobile by buying the van with the kitchen so that he could bring the food directly to his clients in what David calls the Ritz-Carlton of food trucks.

We also talk about how David has evolved his financial planning services for clients, including how David has largely eschewed relying on traditional planning software and instead, built his value proposition directly around the ongoing and never-ending financial planning tasks that his clients need his help to implement, how David built his own custom portals for each client through Microsoft SharePoint to help clients track their financial planning progress over time, and why David has decided to evolve his business model towards charging ongoing planning fees as a percentage of client income for his financial planning task support, in addition to AUM fees where his clients need their portfolios managed.

And be certain to listen to the end where David shares his own journey through the advice business from how he made the transition from being a chef and doing a brief stint at a software company before getting started as a life insurance agent, why David ultimately decided to leave the broker-dealer world and structure his firm as an independent RIA instead, and why David believes that a chef who cooks for his clients in addition to providing them financial advice has been so effective at deepening his client relationships.

So whether you're interested in learning more about why David decided to join his talents as a chef and as a financial advisor into a successful business, why he opts for an almost subscription-style fee model, or how he designs his financial plans with a task-oriented approach, then we hope you enjoy this episode of the Financial Advisor Success podcast.

Traditionally, most financial advisory firms’ business models have been centered around managing their clients’ investment portfolios. Even for firms that offer comprehensive financial planning, investment management is often an important – and, for firms that charge fees on an AUM basis, required – part of the firm’s services. However, there is a segment of potential clients who are not interested in delegating their investment management responsibilities to an advisor, but who are seeking professional guidance on actions that they can take and implement on their own – providing an opportunity for advisors to build a sustainable business offering “Advice-Only” financial planning, without the investment management.

In this guest post, Cody Garrett, CFP – founder of Measure Twice Financial, an Advice-Only financial planning firm – writes about what it means to provide Advice-Only financial planning, the types of clients who engage with his services, how Advice-Only advisors get paid, and how to make it a sustainable business model. Additionally, Cody provides a template for a comprehensive Advice-Only financial planning process that he developed in the course of building his own practice.

Advice-Only financial planning generally serves clients who are comfortable performing investment management tasks on their own, but who have questions about their own situations and strategies that require more personalized advice than YouTube videos or personal finance websites can provide. With most advisory firms still requiring clients to give up control over their investments just to get ‘in the door’, advisors who provide personalized financial planning – while allowing the client to manage their own assets – are highly sought out by these “Do-It-Yourself” (but not “Learn-It-Yourself”) investors.

For advisors who offer Advice-Only planning, the sustainability of the model ultimately depends on how many clients the advisor can (or wants to) serve, and how much revenue from each client they can realize. But because their fees are tied to their advice rather than asset management, Advice-Only advisors can charge a level of fees that reflect the value of the advice that they give – meaning that, for advisors who can provide high-value financial advice to clients with complex needs (and charge fees commensurate with that value) the Advice-Only model can be not just sustainable, but can also give the advisor the flexibility to control both their schedule (since it is not dictated by the schedule tethered to the working hours of the financial markets) and their own income (which does not need to depend on their clients’ asset levels).

Ultimately, for advisors who are passionate about giving comprehensive financial advice – but less so about managing assets – Advice-Only planning is a way to serve clients whose needs align with the advisor’s own expertise and ability to provide value. And because so (relatively) few firms currently offer Advice-Only planning, the firms that do provide it can take advantage of the growing demand for Advice-Only planning to differentiate themselves from traditional AUM-based firms and build a sustainable, flexible advice-based practice!

When it comes to retaining clients, financial advisors benefit from focusing on gaining both the client's confidence and trust. Because while a client may be confident that an advisor can develop a workable financial plan, they will not feel compelled to stay with the advisor unless they can also trust that their advisor has their best interests at heart throughout the process. And even though it is important to have a well laid-out financial plan, it is equally (if not more!) important for advisors to understand the client’s underlying motivation to ensure the plan is relevant and to help clients stay on track with their financial goals. To this end, a statement of financial purpose helps the advisor to create a meaningful plan for the client, and also helps the client stay focused on taking action on the plan and staying the course.

In our 75th episode of Kitces & Carl, Michael Kitces and client communication expert Carl Richards discuss the difference between a “statement of financial purpose” and a “mission statement,” the psychology behind why a statement of financial purpose helps to instill clients with confidence and trust in their advisors, and the importance of crafting statements of financial purpose by first helping the client understand their own “financial why.”

As a starting point, it is important for advisors to begin the financial planning process by understanding the deeper reasons that explain why their clients are seeking advice in the first place. By encouraging clients to take time to carefully reflect on what it would mean for them to achieve their financial goals, financial advisors can discover insight into the client’s motivation to help them craft a relevant and meaningful statement of purpose (written in the client’s own words) that crystallizes why the financial plan is meaningful and important to the client.

Merely creating the statement of financial purpose isn’t enough, though, as clients need to review, reflect upon, and update it periodically, using it as a guide to steer the financial plan, keeping it on track. Advisors and clients can use the statement of purpose as a reminder that all the financial work being done is indeed serving a greater purpose. Additionally, a statement of financial purpose creates an opportunity for advisors to gain trust with clients, by reassuring them that what matters most to them is of paramount importance, and that following their plan (and sticking to it even through the most turbulent times) will help them attain their financial goals.

Ultimately, the key point is that a statement of financial purpose is a living document that helps clients stay focused on their most important goals and encourages them to stick to their plan. At the same time, it also helps to foster greater client trust and confidence in their advisors, facilitating stronger and more open communication channels, which presents advisors with the added bonus of better and deeper connections with their clients!

According to the American Psychological Association, nearly 2/3 of Americans rate money and work as significant sources of stress in their lives. And because money is such a common source of stress, as well as a difficult or uncomfortable topic for many to discuss, we often tend to seek ways to minimize consciously thinking of how we use money (such as by opting for cash-free forms of payment). But people who don’t retain at least some awareness of their spending may subconsciously use other people's behavior as a guide to making money decisions, instead of consciously making choices based on their own personal values and priorities.

In this guest post, Derek Hagen – Founder of Money Health Solutions, a financial therapy and financial life planning firm – discusses how financial advisors can develop a Financial Purpose Statement for their clients to use by helping them examine their relationship with money and identifying their most meaningful goals. Furthermore, he explains how the Financial Purpose Statement can guide clients to live their (financial) lives with deliberation, ultimately helping them to (re-)align their behavior with what matters most to them!

At its core, a Financial Purpose Statement consists of a simple statement that crystallizes the purpose of money in the client’s life. To develop a relevant Financial Purpose Statement, an individual must reflect deeply on the kind of life they would like to have and the person they want to be. Advisors have several tools they can use to help clients examine these ideas and identify their most meaningful values. Some of these include the Klontz/Kahler/Klontz Life Aspirations exercise, which helps individuals consider their ideal life; the Miller/Rollnick Values Cards, which create a systematic process to prioritize meaningful personal values; and George Kinder’s Life Planning Questions, which aim to reveal important life priorities by asking clients to contemplate their own mortality.

Ultimately, Financial Purpose Statements can distill an individual’s values and priorities into an easily accessible reminder that can help them make spending decisions in alignment with what really matters most to them. And by helping clients to develop their own Financial Purpose Statements, advisors can encourage their clients to get clear on what their most important priorities are and guide them toward making the right financial decisions, helping clients live happier lives and achieve their most important goals with clarity and intention!

Welcome back to the 259th episode of the Financial Advisor Success Podcast!

Welcome back to the 259th episode of the Financial Advisor Success Podcast!

My guest on today's podcast is Patricia Houlihan. Patti is the Founder of Houlihan Financial Resource Group, an independent RIA based in the Washington DC area that oversees $345M in assets under management for 150 client households.

What's unique about Patti, though, is the way she’s implementing an internal succession plan with her son and a second advisor, focusing not necessarily on exiting herself from the business and maximizing the value of the sale – because as Patti notes, you can’t take it with you anyway – but instead on ensuring continuity of management and continuity of service for clients so that Patti doesn’t have to actually retire anytime soon at all.

In this episode, we talk in depth about how Patti’s internal succession plan has evolved over the years after clients began to ask her when she was going to retire (and started to highlight their own concerns about how the firm would service them after Patti was gone), the way Patti implemented a team approach where all three advisors of the firm have been in on every client meeting for years so clients have a trust relationship with more than just Patti, and how there hasn’t been any issue implementing a succession plan where Patti’s name is part of firm name – Houlihan Financial Resource Group – because the whole point is that the firm will live as an ongoing concern beyond her (and as Patti notes, if at that point the successors want to change the name, that will be their prerogative anyway!).

We also talk about how Patti structures her financial planning engagements with clients, including why Patti insists that every client needs to go through the details of their household spending as part of the planning process, why despite some naysayers about Monte Carlo analysis, as a former math teacher herself, Patti views it as foundational to having better conversations with clients about retirement, and why Patti prefers to talk about client risk tolerance, not in terms of tolerance for market declines, but instead translates it into the real dollar amount the client would potentially lose in a bear market to make sure they’re really comfortable to have that much at stake.

And be certain to listen to the end, where Patti shares what it was like getting started as a female financial planner in the 1980s when, as Patti puts it, it was very much a “man’s world” in the brokerage industry at the time, how Patti sought to reinforce her own expertise and credibility in her early years by becoming a teacher in a CFP program, and why ultimately the key to success as a financial advisor is all about building your own self-confidence first.

And so whether you’re interested in learning about Patti’s decision to opt for an internal succession plan (rather than selling her firm when she retires), her familial approach when relating to clients, or how Patti focused on her confidence and self-worth to navigate her way to success, then we hope you enjoy this episode of the Financial Advisor Success podcast, with Patricia Houlihan.

Read More...

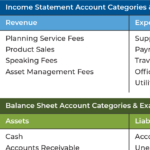

Financial advisory firm owners often rely on their firms' financial data to make decisions for their businesses. But the quality of that data – how it is organized and how much detail it provides about the firm's activities – can greatly affect the firm owner's ability to make good, informed decisions. The firm's Chart of Accounts is a categorized list of every type of transaction that the firm encounters and provides the foundation on which the firm's accounting and bookkeeping systems are organized. It is the key for consistent and accessible data that gives a clear picture of the firm's financial health. A good Chart of Accounts, therefore, can provide the firm owner with insightful data, enabling better decision-making about the firm's future.

The first step towards building an effective Chart of Accounts is to understand how different types of business transactions are accounted for. All business transactions can be sorted into one of five different categories: Assets, Liabilities, Equity, Income, or Expenses. These high-level categories are further divided into subcategories – the "Accounts" in the Chart of Accounts – that are specific to the individual firm's operations. Which means that firm owners have a great deal of flexibility when deciding how many (and which) Accounts should be used to track their firms' financial data.

But with the ability to build a customized Chart of Accounts comes the question of how to build one that leads to making better business decisions. A well-designed Chart of Accounts can be used to generate financial data that provides clear details about how different areas of the firm are performing and where improvements can be made. It should also make it possible to participate in (and compare with) industry benchmarking studies to evaluate the firm's performance alongside its peers, which provides another useful approach for owners to gauge their firms' financial health.

For example, by separating "Direct" expenses – those expenses involved in generating revenue for the firm, such as advisor compensation (including compensation for advisory services provided by owners themselves) – from the "Overhead" expenses of the firm's day-to-day operations, owners can glean insightful data that gives a clearer picture of the firm's profitability. For solo practices, this can even help to show whether the firm actually is profitable after accounting for the owner's work as an advisor.

Because it takes time to build an entirely new Chart of Accounts from scratch, we've provided a downloadable template that includes standard transaction categories relevant to most advisory firms and that can be imported into the firm's accounting software. The template categories align with major industry benchmarking studies, but they can also be adapted to suit the needs of individual advisory firm owners.

Ultimately, the point of the Chart of Accounts is not just to have a system for organizing the firm's financial data, but to be able to access and use that data, to make the firm even better. And by assessing the level of organization and detail that is most relevant for the firm, firm owners can ensure that their firm's financial data will help them make the most well-informed decisions for their business!

Set Password

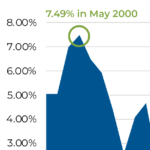

Fixed income investments are an important component in a portfolio because of their ability to cushion against equity market losses. However, when it comes to abundant returns, fixed income holdings have not had much luck during the low-interest-rate environment of the past few years. Accordingly, those seeking higher returns from their bond holdings have had to venture into less secure instruments, such as high-yield “junk” bonds and other alternative-fixed income holdings. Making matters worse, the recent spike in inflation means that many fixed income investments are earning a negative real yield. However, this is not bad news for all fixed income instruments, as this increase in inflation has made the rarely used Federal Series I Savings Bond (or, more simply, the “I Bond”) significantly more attractive for investors.

I Bonds are offered via the Treasury Department and are backed by the U.S. government. They can be purchased through the TreasuryDirect website, and such purchases are limited to $10,000 annually per person. What makes I Bonds unique is their interest structure, which consists of a combined “Fixed Rate” and “Inflation Rate” that, together, make a “Composite Rate” – the actual rate of interest that an I Bond will earn over a six-month period.

While the current Fixed Rate for newly purchased I Bonds is 0%, the Inflation Rate for I bonds purchased before May 1, 2022 is an annualized 7.12%, meaning the Composite Rate is also an annualized 7.12% (the highest rate of I Bonds since May 2000!) for the first six months that the I Bond is held (after which a new Composite Rate will be determined by any change to the Inflation rate). While I Bonds have a 30-year maturity, they can be redeemed after being held for at least 12 months. Investors who redeem I Bonds between 12 months and 5 years after issue will forfeit the last 3 months of interest, but I Bonds held for more than 5 years can be redeemed at their current value.

The $10,000 annual limit on I Bond purchases restricts their benefit for those with larger portfolios, but there are several ways investors could increase the amount purchased at the current (very favorable) Composite Rate. For example, because the annual limit is a calendar-year limit, individuals could purchase $10,000 worth of I Bonds before January 1, 2022, and then an additional $10,000 between January 1 and April 30, 2022. Which means a couple could purchase a combined $40,000 worth of I Bonds and receive the annualized 7.12% Composite Rate for the first six months the bond is held. In addition, I Bonds can also be purchased for children or by trusts and estates, which could further increase the amount purchased. Finally, paper I Bonds can be purchased using a tax refund up to a $5,000-per-return limit, which is in addition to the $10,000 annual limit on I Bonds purchased through the TreasuryDirect website.

Ultimately, the key point is that there is a limited amount of time for investors to purchase I Bonds at their very favorable Composite Rate of 7.12%, especially if they want to maximize the amount purchased for the 2021 and 2022 calendar years. In the current environment of low-interest rates and high inflation, I Bonds represent a potential opportunity for investors to increase the yield for a portion of their fixed income portfolio!

Stay In Touch

This browser is no longer supported by Microsoft and may have performance, security, or missing functionality issues. For the best experience using Kitces.com we recommend using one of the following browsers.