One of the most important aspects of emotional wellbeing is having a feeling of control over one’s time. Indeed, financial advisors often describe one of the benefits of financial planning as helping people take control of their time by giving them the financial freedom to do what they enjoy. And likewise, for advisors themselves, one of the ways to stay happy and thriving is to have the ability to spend time doing what one finds is most valuable or fulfilling.

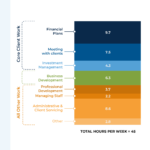

The 2021 Kitces Research Report on What Actually Contributes To Advisor Wellbeing reinforced the idea that the happiest advisors feel in control over their time. Study data showed that ‘Thriving’ advisors – those who reported high levels of overall wellbeing – spent more time on ‘core’ client activities (such as client meetings and developing financial plans) and less time on other activities like administration and back-office tasks when compared to ‘Struggling’ advisors who reported lower wellbeing. Thriving advisors also worked fewer hours each week than their struggling counterparts, suggesting that they not only spent more time on fulfilling client work but also had more time to devote to fulfilling pursuits outside work.

But it wasn’t just the hours spent on each task that mattered for advisor wellbeing. The amount of autonomy that advisors felt over how they spent their working hours – that is, their ability to choose what tasks they worked on over the day – led to them being able to actually spend their time doing work they enjoyed. And while the ability to enjoy this autonomy might be dictated by some factors (like experience) that are out of the advisor’s control, there are methods that all advisors can use to optimize how they manage their schedule, which could make enough of a difference to see a meaningful improvement in wellbeing.

One strategy advisors can use is time blocking – i.e., blocking off stretches of time in one’s calendar for specific tasks or even for a single project. Creating this focused time not only helps eliminate distractions and inefficiencies caused by frequently bouncing between tasks; it can also make the advisor more efficient and effective at their tasks when they are immersed and engaged in their work without interruption.

There are several ways that advisors can implement time blocking in their work. ‘Theme Days’ give each day of the week a specific purpose, so tasks can automatically be sorted into the day they ‘belong’ to. Alternatively, the ‘Ideal Week’ method incorporates business and personal goals for advisors who want to work less than the traditional workweek. And ‘Surge Meeting’ schedules block off certain months or weeks of the year for advisors to get in all their client meetings, freeing up the rest of the year for other projects or even for time off.

Regardless of the method, time blocking works best when the advisor can remain undistracted by other tasks. This might require some creativity in finding ways to eliminate distractions and organize tasks to ensure they are dealt with at an appropriate time rather than buried in an inbox. Ultimately, though, it may require some fine-tuning (and practice!), time blocking can be the path to achieving greater autonomy – and better wellbeing! – in the year ahead.

Welcome back to the 315th episode of the Financial Advisor Success Podcast!

Welcome back to the 315th episode of the Financial Advisor Success Podcast!

Welcome back to the 311th episode of the Financial Advisor Success Podcast!

Welcome back to the 311th episode of the Financial Advisor Success Podcast!